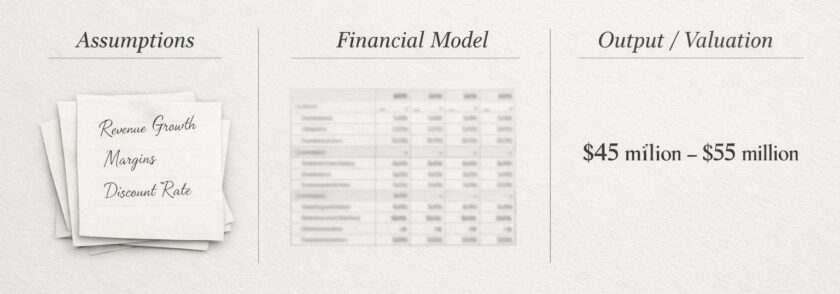

Financial models organize assumptions into structured outputs, but remain dependent on underlying judgments.

A well-built financial model tends to feel convincing.

Everything lines up. Assumptions are neatly laid out. The outputs look precise — sometimes even overly precise. It creates a quiet sense of confidence: if the model is clean, the answer should be reliable.

That belief is where things start to go wrong.

The issue isn’t the model itself. It’s what we expect the model to do.

A financial model doesn’t “find” value. It reflects a view — structured into numbers, made internally consistent, and presented with clarity. That may sound like a small distinction, but it changes how every output should be read.

Why This Matters for Students

Most students learn modeling as a technical exercise.

You build the statements. Link everything properly and arrive at a valuation.

This structured approach feels similar to how to analyze a US stock without too many metrics, where process creates clarity but does not replace judgment.

But that expectation doesn’t hold in practice.

Modeling doesn’t remove uncertainty. It organizes it.

That difference matters more than it appears. In real analysis, the outcome depends less on how well the model is built and more on how the business is interpreted.

Two students can work with the same structure and still reach different conclusions. Not because one made an error — but because they didn’t make the same assumptions.

What Models Appear to Do (The Surface View)

At a glance, financial models seem straightforward.

Inputs go in. Calculations happen. Outputs come out. The flow feels deterministic — almost like a machine.

Take a basic DCF setup:

- Revenue grows steadily

- Margins stabilize over time

- Capital requirements follow a pattern

- A discount rate brings everything back to present value

Put this together, and the model produces a valuation range. If that number sits above the market price, it feels like a clear signal.

On paper, everything works.

That’s precisely why it can mislead.

Where Surface-Level Understanding Breaks Down

The structure of the model is rarely the problem.

What sits inside it is.

Every input carries a view about the future — whether explicitly acknowledged or not. Growth assumes something about demand. Margins assume something about competition. Capital intensity says something about how much reinvestment the business requires. Even the discount rate reflects a judgment about risk.

None of these are neutral.

They are decisions.

The model doesn’t challenge them. It accepts them and moves forward.

This feels fine — until small changes begin to matter more than expected.

Adjust growth slightly downward. Increase the discount rate by a point or two. The output shifts, sometimes materially.

Nothing “broke” in the model.

The assumptions moved.

DCF models convert assumptions into valuation outputs using structured calculations.

A discounted cash flow model explained in basic terms can help understand the mechanics, but it does not address the assumptions embedded within it.

That is where deeper analysis begins.

A More Accurate Framework: Models as Translation Tools

It helps to think of financial models differently.

They don’t answer questions. They translate views.

Whatever you believe about a business — its growth, its resilience, its risks — the model converts that into numbers. That’s all it does.

Which leads to a better question.

Instead of asking whether the model is correct, it’s more useful to ask:

What has to be true for this model to make sense?

If margins are expected to hold, what supports that view, and if growth appears stable, what prevents disruption? Similarly, if capital needs seem manageable, what ensures they remain that way?

The model doesn’t verify any of this.

It assumes it.

When Financial Models Work Well

There are situations where modeling becomes more useful.

Typically, these involve businesses with relatively stable characteristics — predictable demand, consistent cost structures, limited structural change. In such cases, past behavior provides some guidance about the future.

Here, models can help frame expectations.

They allow you to test scenarios, understand sensitivity, and organize thinking in a structured way. The outputs still depend on assumptions, but the range of outcomes tends to be narrower.

That makes the exercise more grounded.

Not certain — but more manageable.

When Models Create False Confidence

The limitations show up more clearly when uncertainty increases.

Early-stage companies, cyclical industries, or businesses facing structural shifts rarely behave in predictable ways. Yet the model still produces clean, precise outputs.

That contrast is where problems start.

The numbers look exact. The underlying reality isn’t.

A common response is to add more detail. Break forecasts into finer pieces and introduce more assumptions.

This connects directly to when valuation models help and when they give false confidence, where added complexity often creates the illusion of accuracy.

More detail doesn’t necessarily improve reliability.

Sometimes it just makes the uncertainty harder to see.

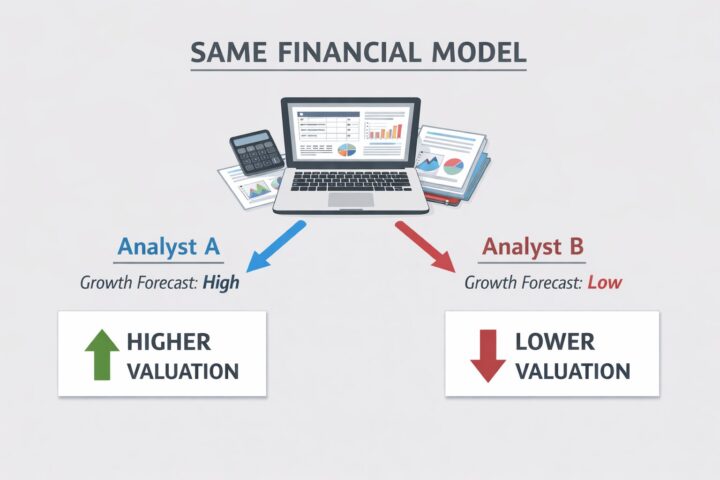

Two Analysts, Same Model, Different Conclusions

Consider two students working on the same company.

They build identical model structures. Use similar data. Follow the same process.

Yet the conclusions differ.

One believes the company’s position will strengthen — growth remains healthy, margins hold, risk feels contained. The other sees pressure building — growth slows, margins compress, uncertainty increases.

The model reflects both views without resistance.

Same framework. Different inputs. Different outcomes.

Neither model is technically wrong.

The difference comes from how the business is interpreted.

Models don’t eliminate disagreement.

They make it visible.

What Most Students Miss

Students often focus on what’s easiest to check — formulas, structure, and formatting.

This reflects why most beginner stock analysis guides fail in real markets, where process replaces judgment without improving outcomes.

In reality, a few key assumptions drive most of the result. Growth rates, margins, reinvestment, and discount rates tend to carry disproportionate weight.

Understanding that concentration is more important than perfecting structure.

A simple model, built on thoughtful assumptions, often tells you more than a complex one built on unexamined inputs.

This is where confusion creeps in.

Complexity feels like sophistication.

It isn’t always.

What Most Articles Don’t Explain Clearly

A lot of financial modeling content focuses on construction.

Step-by-step guides. Templates. Formula explanations. These are useful, especially early on. But they quietly reinforce the idea that modeling is mainly technical.

That’s only part of the picture.

In practice, most models follow similar structures. The real difference lies in how assumptions are formed — and how comfortable the analyst is in questioning them.

This is rarely emphasized.

As a result, it’s possible to become very good at building models without becoming equally good at interpreting them.

What Students Should Stop Focusing On

There are a few habits that seem productive but often aren’t.

Spending excessive time refining structure. Adding layers of detail that don’t change the conclusion. Treating valuation outputs as definitive answers rather than conditional estimates.

These tendencies come from a reasonable place.

They create a sense of precision.

But precision and certainty are not the same thing.

A model can be technically perfect and still lead to the wrong conclusion — simply because the assumptions behind it are fragile.

This mirrors why a low pe ratio often misleads retail investors, where surface-level signals appear convincing but hide deeper uncertainty.

Key Takeaways

Financial models don’t produce answers. They organize assumptions.

Every output reflects a view about how a business will evolve. Change that view, and the output changes with it.

Two well-built models can disagree — without either being incorrect.

The value of modeling lies in making uncertainty visible, not in removing it.

FAQ (For Students & Beginners)

Because they interpret the business differently. The structure may be similar, but the inputs are not.

No. It gives a value based on assumptions. If those assumptions change, the valuation changes as well.

Not necessarily. More complexity often adds more assumptions, which can reduce clarity instead of improving it.

Understanding the business and its drivers. The model reflects your thinking — not the other way around.

That it produces objective answers. In reality, it produces structured outcomes based on subjective assumptions.

Boundaries & Context

This does not mean financial models are unreliable.

They are essential tools and widely used across finance.

But they have limits.

A model can look precise.

A business can still be uncertain.

Recognizing that gap is where more disciplined analysis begins.