Navigating India’s evolving tax system is no longer a once-a-year job — it demands smart decisions well in advance.

Following the latest Budget 2025 announcements, salaried individuals must make an important choice:

Continue with the traditional Old Tax Regime or shift to the simpler New Tax Regime?

Your selection could either maximize your savings or lead to silent financial leakage over time.

In this detailed guide, we’ll walk you through everything — slab rates, real salary calculations, marginal relief concepts, and what happens if your income crosses ₹12 lakh by even a single rupee.

Let’s understand it step-by-step.

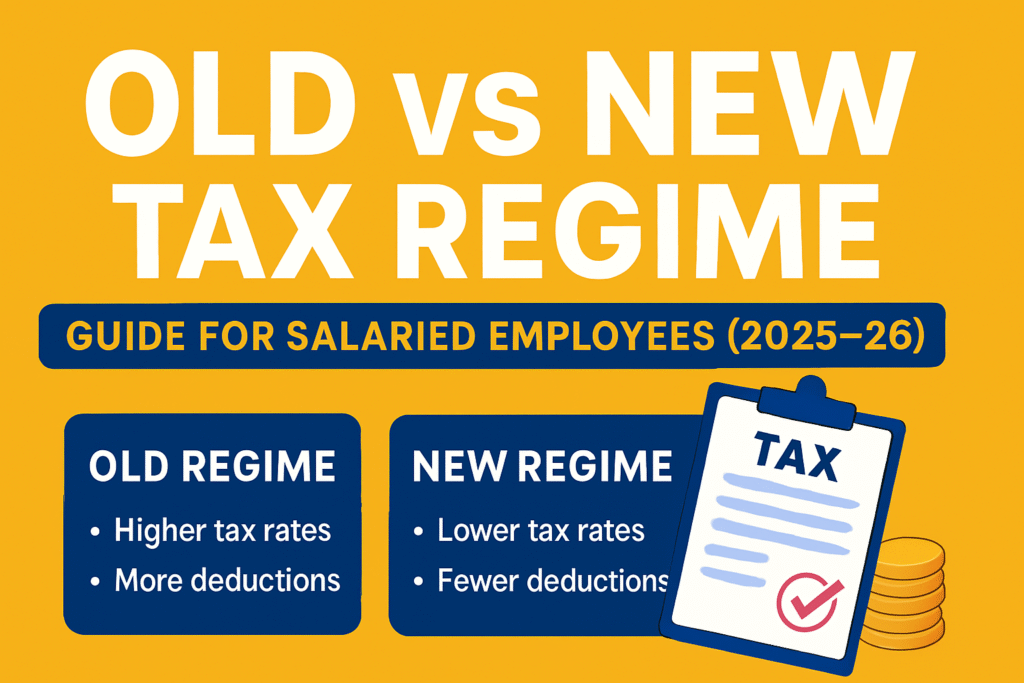

📚 What is the Fundamental Difference Between Old and New Tax Regimes?

Here’s the simple version:

- Old Tax Regime:

You get to claim multiple deductions and exemptions like:- ₹1.5 lakh investment under Section 80C

- Medical insurance premium under Section 80D

- House Rent Allowance (HRA) exemption

- Interest paid on home loans (Section 24b)

- Leave Travel Allowance (LTA)

- New Tax Regime:

Offers lower tax rates, but with minimal deductions. Only the standard deduction (₹75,000) and some employer-side contributions like NPS/EPF are allowed.

✅ The focus is on simplicity — no investment proofs, no complex documentation.

📈 New Tax Slabs for FY 2025–26 (Applicable under New Regime)

| Income Slab | Tax Rate |

|---|---|

| Up to ₹4 lakh | Nil |

| ₹4,00,001–₹8,00,000 | 5% |

| ₹8,00,001–₹12,00,000 | 10% |

| ₹12,00,001–₹16,00,000 | 15% |

| ₹16,00,001–₹20,00,000 | 20% |

| ₹20,00,001–₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Source: Official Income Tax Slabs and Notifications Source.

🎯 What New Benefits Were Introduced in Budget 2025?

Two major changes have made the New Regime extremely attractive:

| Particulars | Amount (FY 2025–26) |

|---|---|

| Standard Deduction | ₹75,000 |

| Section 87A Rebate | ₹60,000 |

✅ If your net taxable income (after ₹75,000 standard deduction) stays within ₹12 lakh, you qualify for a ₹60,000 rebate — effectively reducing your final tax payable to zero.

🧮 Real-Life Example 1: Salary of ₹12.75 lakh

Suppose your gross salary is ₹12,75,000.

Step-by-step:

- Gross Salary = ₹12,75,000

- (–) Standard Deduction = ₹75,000

- ➡️ Net Taxable Income = ₹12,00,000

Tax Calculation:

| Taxable Slab | Rate | Tax Amount |

|---|---|---|

| 0–₹4 lakh | 0% | ₹0 |

| ₹4–8 lakh | 5% | ₹20,000 |

| ₹8–12 lakh | 10% | ₹40,000 |

- Basic Tax = ₹60,000

- 87A Rebate = ₹60,000

- Final Tax = ₹0

✅ Congratulations — you pay zero tax if your salary after standard deduction fits within ₹12 lakh!

⚠️ Real-Life Example 2: Salary of ₹13 lakh

Now imagine your gross salary is ₹13,00,000.

Step-by-step:

- Gross Salary = ₹13,00,000

- (–) Standard Deduction = ₹75,000

- ➡️ Net Taxable Income = ₹12,25,000

Tax Calculation:

| Taxable Slab | Rate | Tax Amount |

|---|---|---|

| 0–₹4 lakh | 0% | ₹0 |

| ₹4–8 lakh | 5% | ₹20,000 |

| ₹8–12 lakh | 10% | ₹40,000 |

| ₹12–12.25 lakh | 15% | ₹3,750 |

- Basic Tax = ₹63,750

- Cess @4% = ₹2,550

- Total Tax = ₹66,300

🛡️ How Marginal Relief Saves You

Here’s the trap many employees fall into:

By earning just ₹25,000 extra, they lose the entire ₹60,000 rebate and suddenly face ₹66,300 tax!

Luckily, Marginal Relief is designed to protect you.

Let’s see:

- Extra Income above ₹12 lakh = ₹25,000

- Extra Tax without relief = ₹66,300

Since extra tax > extra income, Marginal Relief applies.

Thus:

- Your final tax payable becomes just ₹25,000 (equal to the extra income earned).

✅ Marginal relief ensures you don’t get unfairly penalized for marginal increases in salary!

📋 Salary vs Tax Payable (Including Marginal Relief)

| Gross Salary | Net Taxable Income | Marginal Relief Applicable? | Final Tax Payable |

|---|---|---|---|

| ₹12.75 lakh | ₹12 lakh | Yes (87A rebate) | ₹0 |

| ₹13 lakh | ₹12.25 lakh | Yes (Marginal Relief) | ₹25,000 |

| ₹13.5 lakh | ₹12.75 lakh | No | ₹38,400 (approx.) |

🏡 When Does the Old Regime Still Make Sense?

If you’re claiming multiple deductions such as:

- ₹1.5 lakh under Section 80C

- ₹25k–₹75k under Section 80D (health insurance)

- HRA exemptions for rented accommodation

- Interest on home loans under Section 24(b)

then the Old Tax Regime could still offer better savings despite higher tax rates.

📝 Pro Tip:

Always total up your available deductions before deciding.

📢 Important Warning: Salary Above ₹12 Lakh?

If your taxable salary crosses ₹12 lakh by even ₹1 after standard deduction:

- You lose the ₹60,000 rebate immediately.

- Your tax liability increases steeply.

- You must depend on Marginal Relief if eligible.

✅ Always calculate net taxable income, not just gross salary, while doing tax planning.

🙋 Frequently Asked Questions (FAQs)

1. Can salaried individuals switch between tax regimes every year?

✅ Yes! You can opt for a different tax regime every financial year if you are a salaried taxpayer.

2. Is Standard Deduction available under both regimes?

✅ Absolutely. ₹50,000 under the Old Regime and ₹75,000 under the New Regime (from FY 2025–26).

3. What deductions are allowed under the New Regime?

✅ Only a few:

- Standard Deduction (₹75,000)

- Employer’s NPS/EPF contributions

- Agniveer Corpus Fund contribution

4. Should I still invest even if I choose the New Regime?

✅ Yes! Smart investments build wealth over the long term — not just for tax savings.

🎯 Conclusion: Choose Smartly, Choose Wisely

The New Tax Regime is a great fit for those who prefer simplicity and don’t rely much on deductions.

If your taxable salary remains within ₹12 lakh after deductions, it could mean zero tax payable.

However, if you are actively investing or have heavy deductions lined up, the Old Regime could still offer better overall savings.

✅ Run side-by-side calculations.

✅ Consult a financial advisor if needed.

✅ Keep an eye on the ₹12 lakh slab!

Today’s smart choice will compound into tomorrow’s financial freedom.

Read other popular article: Trump Tariffs 2025: Temporary Relief for India Amid Global Trade Tensions

Küçükçekmece su kaçak tespiti Dinleme cihazları, kazma yapmadan yeraltı boru kaçaklarını tespit edebilir. http://www.ahc-international.at/wordpress/?p=3977

Harbiye su kaçak tespiti Beylerbeyi su kaçağı tespiti: Beylerbeyi’nde su kaçağına garantili çözüm. https://ukerala.com/2012/

Yenidoğan su kaçak tespiti Tuzla su kaçağı tespiti: Tuzla’da su kaçağını kısa sürede tespit ediyoruz. http://www.tecnoac.com/?p=13583

Kısıklı su kaçağı tespiti Su kaçağı tespiti, çevre dostu ve su kaynaklarını koruyucudur. https://learn.kegerator.com/author/kacak/

nokta atışı su kaçak tespiti Kozyatağı su kaçağı tespiti: Kozyatağı’nda su kaçağını hızlıca buluyoruz. http://turkiyeplatformu.com/uskudar-su-tesisatcisi.html

Çatalca Merkez su kaçak tespiti Kozyatağı su kaçağı tespiti: Kozyatağı’nda su kaçağını hızlıca buluyoruz. https://relxnn.com/?p=39495

перепродажа аккаунтов продажа аккаунтов соцсетей

биржа аккаунтов площадка для продажи аккаунтов

площадка для продажи аккаунтов купить аккаунт

платформа для покупки аккаунтов купить аккаунт с прокачкой

купить аккаунт маркетплейс для реселлеров

продажа аккаунтов соцсетей аккаунты с балансом

купить аккаунт продать аккаунт

гарантия при продаже аккаунтов аккаунты с балансом

перепродажа аккаунтов покупка аккаунтов

аккаунт для рекламы магазин аккаунтов

заработок на аккаунтах аккаунт для рекламы

аккаунт для рекламы маркетплейс аккаунтов

маркетплейс аккаунтов соцсетей https://pokupka-akkauntov-online.ru/

Marketplace for Ready-Made Accounts Secure Account Sales

Account Purchase Account trading platform

Accounts for Sale Account market

Account Trading https://buyaccountsmarketplace.com

Secure Account Purchasing Platform Ready-Made Accounts for Sale

Account market Account Purchase

Online Account Store Account Buying Platform

Purchase Ready-Made Accounts Account market

Sell Pre-made Account Account Trading Platform

Account Sale Account exchange

account market account trading service

ready-made accounts for sale account trading

accounts marketplace account exchange service

online account store accounts market

account selling platform account exchange

profitable account sales marketplace for ready-made accounts

account trading platform secure account sales

Well written and inspiring! Keep up the great work.

ready-made accounts for sale account marketplace

buy pre-made account find accounts for sale

marketplace for ready-made accounts guaranteed accounts

account market ready-made accounts for sale

database of accounts for sale find accounts for sale

account buying platform find accounts for sale

gaming account marketplace account market

Thanks for sharing! I learned something new today.

account market account trading

verified accounts for sale account exchange service

social media account marketplace account trading platform

sell accounts marketplace for ready-made accounts

account trading account marketplace

sell accounts buy account

accounts for sale account trading

account exchange account trading platform

Looking at slot game return rates, platforms like Jilislot stand out by combining AI insights with player-friendly design, offering a smart edge in the competitive online gaming world.

database of accounts for sale account trading service

online account store verified accounts for sale

buy pre-made account ready-made accounts for sale

account buying service https://accounts-offer.org

account trading service accounts marketplace

online account store https://social-accounts-marketplaces.live

profitable account sales https://accounts-marketplace.live

account marketplace https://social-accounts-marketplace.xyz/

buy pre-made account https://buy-accounts.space

purchase ready-made accounts https://buy-accounts-shop.pro/

gaming account marketplace https://buy-accounts.live/

marketplace for ready-made accounts https://accounts-marketplace.online

account acquisition https://social-accounts-marketplace.live

website for buying accounts https://accounts-marketplace-best.pro

маркетплейс аккаунтов https://akkaunty-na-prodazhu.pro/

маркетплейс аккаунтов https://rynok-akkauntov.top

покупка аккаунтов kupit-akkaunt.xyz

биржа аккаунтов https://akkaunt-magazin.online

маркетплейс аккаунтов https://akkaunty-market.live

покупка аккаунтов https://kupit-akkaunty-market.xyz

Sprunki Incredibox brings fresh beats and vibrant visuals to the beloved Incredibox formula. It’s a must-try for fans looking to mix music in new ways. Check out the holiday twist in the Sprunki Christmas Game for a festive spin!

купить аккаунт akkaunty-optom.live

маркетплейс аккаунтов https://online-akkaunty-magazin.xyz/

покупка аккаунтов akkaunty-dlya-prodazhi.pro

продажа аккаунтов https://kupit-akkaunt.online

Great insights! This really gave me a new perspective. Thanks for sharing.

I’m excited to see how AI is reshaping design workflows. Tools like Lovart offer a fresh way to blend creativity with automation-especially cool for turning pixel art into modern visuals. Can’t wait to see it in action!

buy account facebook ads buy facebook ad account

facebook account sale https://buy-ad-accounts.click

buy a facebook ad account facebook ad accounts for sale

facebook ad accounts for sale facebook accounts to buy

Zeytinburnu su kaçağı cihazlı tespit Sızıntıyı hızlıca bulup onardılar, tekrar teşekkürler! https://www.grand-indonesia.com/author/kacak/

buy aged fb account https://ad-account-buy.top

cheap facebook accounts buy facebook accounts

facebook ads account for sale https://ad-account-for-sale.top

buy facebook old accounts https://ad-accounts-for-sale.work

google ads agency accounts https://buy-ads-account.top/

buy google ad threshold account buy google ad threshold account

buy google ads threshold accounts https://ads-account-for-sale.top/

google ads agency accounts https://ads-account-buy.work

buy google ads invoice account https://buy-ads-invoice-account.top

buy google ad threshold account buy google ads threshold accounts

buy google adwords accounts https://buy-ads-agency-account.top

buy old google ads account https://sell-ads-account.click

buy aged google ads account https://ads-agency-account-buy.click

Just like a good blackjack hand, finding the right AI tools takes strategy. The AI Trading Bot Assistant is a solid pick for streamlining smart decisions-definitely one to keep in your deck.

buy business manager https://buy-business-manager.org/

google ads account seller buy old google ads account

fb bussiness manager buy verified bm

buy facebook business managers buy-verified-business-manager-account.org

fb bussiness manager https://buy-verified-business-manager.org

facebook verified business manager for sale https://buy-business-manager-acc.org

buy facebook verified business manager https://business-manager-for-sale.org

buy business manager account https://buy-business-manager-verified.org/

buy facebook business account facebook business manager for sale

If you’re new to slots, give Super Ace a try-its 1024 ways to win and wild card features make it fun and rewarding for casual players like me.

facebook business manager account buy https://buy-business-manager-accounts.org/

tiktok ads agency account tiktok ads account for sale

Thanks for the insightful breakdown! It’s refreshing to see a guide that blends practical tips with immersive storytelling. For those diving deeper into AI tools, I highly recommend checking out Best AI Tools to explore top resources.

buy facebook business manager account verified-business-manager-for-sale.org

tiktok ads agency account https://tiktok-ads-account-buy.org

buy tiktok ads https://tiktok-ads-account-for-sale.org

tiktok ads account for sale https://tiktok-agency-account-for-sale.org

buy tiktok ads https://buy-tiktok-ad-account.org

tiktok agency account for sale tiktok ad accounts

JiliPH really enhances the live dealer experience with its smooth gameplay and variety of slots like Fortune Gems. New players should check out Jilicasino for an easy start!

buy tiktok ads account https://tiktok-ads-agency-account.org

Slot games thrive on RNG, but platforms like SuperPH11 balance fun with fair play. Their diverse titles and smooth interface make for a top-tier gaming experience worth exploring.

tiktok ads agency account https://buy-tiktok-business-account.org

buy tiktok ads accounts https://buy-tiktok-ads.org

Transform your living space with timeless style and function from JASIWAY. Our versatile JASIWAY sofa bed is perfect for hosting guests or relaxing in style—an essential sofa bed for modern living. Add charm and utility to your room with a JASIWAY coffee table, or choose a sleek coffee table that fits any décor. Get organized in style with a JASIWAY dressing table, designed for elegance and convenience—your ideal dressing table awaits. Elevate your entertainment setup with a JASIWAY TV stand, crafted for durability and beauty—every TV stand is built to impress. Redefine comfort with a JASIWAY sofa that blends luxury and practicality. Whether it’s a centerpiece or a cozy spot, the perfect sofa is just a step away. From design to comfort, JASIWAY delivers furniture that fits your life beautifully.

Trying out Super PH was a fun mix of luck and strategy-those wilds really helped boost wins without feeling too complicated. Definitely worth a spin!

Online gaming platforms like JLJLPH are raising the bar with live dealers and secure interfaces. Their slot variety and easy registration process make it a top pick for casual and serious players alike.

我們致力於為全港市民提供安全、專業、有系統的游泳訓練課程。課程涵蓋幼兒、兒童、青少年及成人,從基本漂浮、換氣技巧,到四式泳法(自由式、蛙式、背泳、蝶泳)訓練,一應俱全。無論您居住在將軍澳、觀塘、柴灣、荔枝角、大埔或粉嶺,都可以找到就近的泳池地點上課。每位學員都會由經驗豐富、持牌認可的游泳教練指導,確保在歡樂中學習,在安全中進步。透過我們的游泳班與游泳會,讓學員建立自信、鍛鍊體魄,甚至為將來參加比賽奠定基礎。

The 1024 paylines in SuperPH26 really boost your odds-smart design for a thrilling slot. Check out the action at SuperPH26 Login!

Jili Online really stands out with its AI-powered insights-great for players aiming to boost their odds. The platform’s variety and security make it a top pick for Filipino gamers. Check it out at Jili Online!

Loving the deep dives into team dynamics and player performance-crucial for anyone serious about 11phdream matchups. Keep up the sharp analysis!

Great article! For football bettors looking to enhance their strategy, check out the AI Trading Bot Assistant. It’s a smart tool for optimizing data-driven decisions.

It’s so important to remember enjoyment is key with any online activity. Platforms like phdream22 login seem to prioritize user experience – a good sign! Let’s all play responsibly & keep it fun. 😊 Knowing access is streamlined helps too!

Understanding game mechanics is key to enjoying casino play, and not just relying on luck! Building a solid foundation, like the approach at SuperPH11 Login, can really boost confidence. It’s about smart play, not just chance! 🤔

Mobile gaming is evolving so fast! Seeing platforms prioritize user experience-like optimizing every tap & swipe-is key. Exploring options like PH Login Casino could really elevate playtime & engagement. It’s all about seamless access, right?

Great breakdown of blackjack strategy-really helped me see the game from a new angle. It’s always fun to learn how small decisions can lead to big wins. If you’re looking to try out some of these strategies in action, check out Jili No1 for a smooth and engaging gaming experience.

Great insights! PH987 slot offers a smooth and thrilling gaming experience with top-tier security and a wide range of exciting games to enjoy.

That’s a fascinating point about deliberate practice! Building a solid foundation is key, almost like the registration process at Pinas777 Login – precision matters. Skill mastery takes time & a focused approach, definitely!

Creating Ghibli-style art used to feel out of reach, but now with tools like Ghibli AI, anyone can bring magical scenes to life-no drawing skills needed. What a creative boost!

That’s a fascinating point about game mechanics – really elevates the experience! Seeing platforms like ph987 game focus on strategy and security is impressive. A smooth login is key, too! 🤔

This post really highlights how AI is reshaping creativity. Platforms like AI Ad Creative Assistant make it easier to find tools that actually work for real-world applications.

Altayçeşme su kaçak tespiti Mutfaktaki su sızıntısının kaynağını termal kamerayla buldular. Tezgaha zarar vermeden tamir ettiler. Şükran D. https://x.com/Ustaelektrikci

Ataşehir Mahalleleri: Su kaçağı tespiti için doğru adres olduklarını kanıtladılar. http://banahkhabar.com/author/kacak/

Interesting read! It’s smart how platforms like abc8vip are focusing on making things easy for new players – verification & simple logins are key. Good content! 👍

Esentepe su kaçak tespiti Su kaçağı tespiti için doğru adres olduklarını kanıtladılar. http://siddika-ates-photography.com/author/kacak/

Online gambling requires smart fund management, and platforms like Jili77 offer a secure, user-friendly environment with diverse game options to help players stay in control.

Aydınlı su kaçak tespiti Hızlı servis, uygun fiyatlar. Kesinlikle öneriyorum. https://last-report.com/author/kacak/

kırmadan su kaçak bulma İstanbul Esnek Randevu: Çalışma saatlerimize uygun bir randevu oluşturdukları için teşekkürler. https://ideasofdecoration.com/index.php/author/kacak/

Interesting take! Seeing platforms like ph978 really push boundaries – anticipating what players want before they even know it is key. The future of immersive gaming is definitely here! 🤔

Sultanbeyli su kaçak tespiti Fiyat konusunda dürüstler, sürpriz fatura çıkmadı. https://divinedirectory.com/author/kacak/

Mobile gaming is evolving so fast! It’s all about seamless experiences now, and optimizing for mobile-first is key. I was reading about game ph login and their focus on user behavior – really smart! Definitely a step up for convenience.

Fatih su kaçağı tespiti Silivri su kaçağı tespiti: Silivri’de su kaçaklarına kalıcı çözümler sunuyoruz. https://aipair.io/read-blog/5005

su sızıntısı tespiti Hızlı Ekip: Kocaman bir ekiple geldiler ve işlemi çok hızlı tamamladılar. https://communiti.pcen.org/read-blog/28282

Interesting points on adapting strategy to different stack sizes! Seeing platforms like 78win focus on smooth onboarding is key for new players – tech & tradition blending well. Solid analysis overall!

Çapa su kaçak tespiti İşlerini büyük bir titizlikle yapıyorlar, gönül rahatlığıyla tavsiye ederim. https://viracore.one/read-blog/9472

Arnavutköy su kaçak tespiti Test pompası ile kaçağın kesin yerini bulmaları çok iyiydi. https://www.noifias.it/read-blog/54923

Scratch cards are such a fun, quick thrill! It’s interesting how platforms like SZ777 casino login focus on user journeys – making it easy to engage is key, right? Reducing friction seems smart for boosting those completion rates! 👍

Interesting take on responsible gaming! It’s great to see platforms prioritizing education, especially for newcomers. I noticed phlwin casino offers guided tutorials – a smart approach to building player confidence & understanding game mechanics. Definitely a plus!

Profitez d’une abonnement IPTV exceptionnelle en 2025 avec le meilleur fournisseur Smart IPTV France ! Regardez plus de 63 000 chaînes HD & 4K, accédez à plus de 86 000 films et séries en VOD, et profitez d’une stabilité à 100 % sans interruptions. Regardez vos contenus préférés où que vous soyez, à tout moment et sur n’importe quel appareil : Smart TV, PC, mobile, tablette et plus encore ! Ne manquez plus aucun match, film ou série – optez pour la qualité et la performance d’un smart IPTV premium !

Interesting points! Understanding game fundamentals is key, and a structured approach really helps. Resources like PH365 Login offer that – building skills beyond just luck is crucial for long-term success, especially with evolving strategies.

For baccarat players, understanding patterns is key-just like how JiliOK Login uses AI to enhance gameplay. Their platform offers a refined, immersive experience that’s a cut above the rest.

Basic strategy really shifts your perspective at the blackjack table! Seeing those probabilities makes a huge difference. Just explored jiliboss and their game variety looks fun – a good place to practice! Definitely helps build confidence. 👍

En 2025, la télévision traditionnelle

laisse place à une solution plus moderne, plus riche et plus

flexible : l’abonnement IPTV. Grâce à Smart IPTV France, vous

avez accès à plus de 63 000 chaînes HD/4K et un catalogue impressionnant de 86 000

films et séries en VOD, accessibles à tout moment, sur

tous vos appareils (Smart TV, mobile, tablette, ordinateur ou Android box).

La qualité de diffusion est exceptionnelle, avec zéro interruption et une interface simple d’utilisation.

Ce service s’adresse aussi bien aux passionnés

de sport qu’aux amateurs de cinéma ou aux familles

recherchant des contenus variés. En tant qu’iptv abonné, vous bénéficiez d’un code IPTV sécurisé qui

vous permet de profiter de vos programmes favoris sans limite

géographique. Que vous soyez en France, à l’étranger

ou en déplacement, votre iptv abonnement vous suit partout avec une stabilité remarquable.

Testez gratuitement pendant 24 heures pour découvrir pourquoi Smart IPTV est considéré comme le meilleur iptv en France.

Grâce à un support client réactif et une compatibilité

multi-plateforme, nous garantissons une expérience

premium pour tous nos utilisateurs. Ne perdez

plus de temps avec des services limités : optez dès maintenant pour la performance, la liberté et la richesse de

l’IPTV France nouvelle génération.

Visitez dès maintenant france iptv

et découvrez le meilleur abonnement IPTV en France.

Découvrez la puissance du smart IPTV et transformez votre manière de regarder la télévision. Fini les coupures,

les limites géographiques ou les abonnements coûteux.

Avec un iptv abonnement, vous accédez à des milliers de contenus en un clic.

Compatible avec tous vos appareils, notre service propose plus de 63 000 chaînes et 86 000

contenus VOD disponibles à tout moment. Il vous suffit d’entrer un code IPTV pour débloquer un univers

complet de divertissement, sans installation complexe.

Notre plateforme IPTV France vous assure une diffusion stable, une interface intuitive,

et un support disponible 24h/24. Testez notre service pendant 24h gratuitement et profitez d’une qualité incomparable.

Visitez dès maintenant iptv abonné

et découvrez le meilleur abonnement IPTV en France.

Velibaba su kaçak tespiti Su kaçağı tespiti, çevre dostu ve su kaynaklarını koruyucudur. https://social.instinxtreme.com/read-blog/47603

That’s a great point about volatility! Finding the right balance is key, and platforms like jlboss com seem to offer a huge variety, from classic to modern slots – good for testing different strategies! Quick signup is a plus too.

That’s a great point about responsible gaming – crucial for enjoying platforms like JLBoss! It’s cool they prioritize a smooth experience; easy login with boss jl is a big plus. Finding a balance is key to having fun! ✨

Lottery odds are fascinating, aren’t they? Seeing platforms like 99win Club offer diverse games-from slots to live casino-adds another layer of probability to consider! If you’re exploring options, check out the 99win app download apk for a quick start. It’s interesting how accessibility impacts participation!

Solid analysis! Understanding team form and having convenient access to games is key. The ease of a mobile app like this – check out a jl boss app download – could really change how people engage with betting. Quick logins are a must!

Interesting read! Thinking about how tech is changing things – even in gaming. Seeing platforms like 33wim app focus on streamlined, secure experiences with things like biometric verification is impressive. It’s the future!

It’s easy to get carried away with online casinos! Responsible play is key, & platforms like jl boss games are innovating with tech – secure logins & smart recommendations can help manage your experience. Stay cautious!

Đang quay ở sin88 vn thì đang quay thì bị hết pin, trúng mà không kịp chụp 😭

That’s a really interesting point about game accessibility! Seeing platforms like 99wim game prioritize fast, secure registration with AI is a smart move for wider adoption – less friction is always good! 👍

Tuzla Elektrikçi İşini iyi yapıyor ama biraz geç geldi. Fiyat makul.” http://www.balikesirim.net/firma-rehberi/usta-elektrikci-1088.html

Interesting take on baccarat strategy! Seeing platforms like jl boss slot innovate with smoother deposits (GCash is key!) & diverse games definitely enhances the experience. It’s all about maximizing enjoyment, right?

Dice games are such a fascinating blend of luck & strategy! Seeing platforms like jljlboss download offer diverse options-slots, live dealers-really elevates the experience. Secure onboarding (KYC) is key, too! 👍

It’s fascinating how localized experiences drive engagement – seeing that with platforms like PH987, catering specifically to Filipino players. Secure logins & KYC are key for trust, and checking out the ph987 app download might be a good starting point for exploring that approach!